5 Ways to Stand Out and Boost Black Friday Sales

Black Friday is the day after Thanksgiving, falling on Friday 29th November in 2024. It’s known for being a perfect time for snagging a bargain, opening the...

The taxation of gains and profits that come from offshore accounts is often complex. Note that HMRC can access overseas financial data to unprecedented levels.

In addition to HMRC's access to data, it's "no safe haven" offshore strategy is another important aspect to consider if you're a foreign bank account holder. HMRC has renewed its strategy in 2019 and incorporated punitive penalties for people failing to disclose their offshore accounts.

That means declaring foreign bank accounts to HMRC is of paramount importance. One of the key principles in the UK tax law is that all UK residents must declare their income and profits from their foreign accounts, including those in the UK. In fact, HMRC has launched a campaign against individuals with undeclared overseas income.¹

If you're a foreign account holder, reading this article will help you understand why declaring a foreign bank account to HMRC is mandatory. We will also explain how you can do so.

If you're a business sending more than 100,000 GBP (or equivalent) monthly across different currencies, get in touch with the Wise Business sales team to discuss the best solutions for your needs.

Talk with Wise Business Sales Team 🚀

To avoid possible penalties - As mentioned above, HMRC has warned taxpayers that declaring foreign bank accounts or offshore assets is necessary for the UK residents. They may face penalties if legal authorities come into force. HMRC has set 30th of September as the deadline for all UK taxpayers to declare their foreign profits and income to avoid significant tax penalties.

Requirement to Correct - The new legislation or renewed law 2019 "Requirement to Correct" requires taxpayers in the UK to notify tax authorities about their overseas liabilities pertaining to UK inheritance tax, income tax, and capital gain tax. However, many taxpayers in the UK don't realize that they need to disclose their foreign financial interests.

Under these rules, actions like transferring assets or profits from a foreign country to the home country and buying or renting a property overseas mean the taxpayer has to pay a tax bill in the UK. Even if you live abroad and buy or rent a property in the UK, you will have to declare it to HMRC and pay tax on it.³

If you need to move some funds around to cover your tax liabilities or collect your Foreign Tax Credit Relief, Wise can save you over 60% on international transfer fees compared to most high street banks. It's also up to 19x cheaper than PayPal.

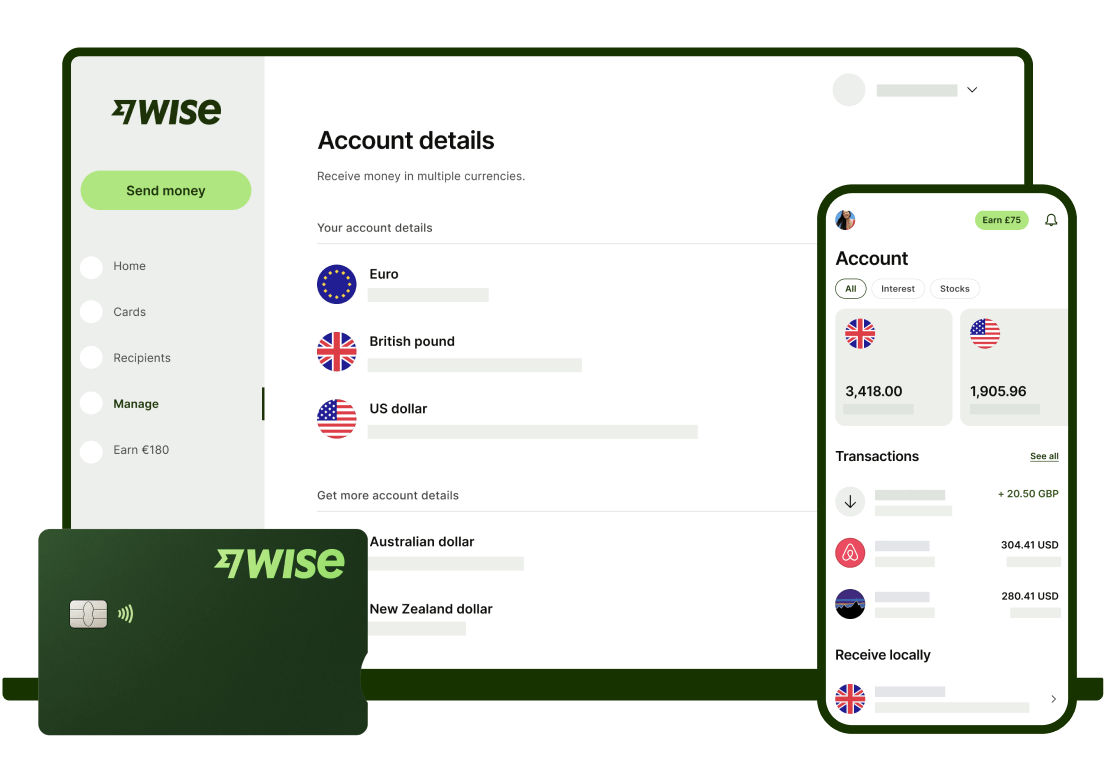

Old-world bank accounts only work properly in one country. They hold money only in one currency. And it gets expensive when you try to use them across borders. Wise's new Multi-currency accounts solve all of this.

Now you can send, receive and organise your money internationally, without crazy fees or even-crazier exchange rates – just a small, fair charge when your money moves between currencies.

To correct tax liabilities, taxpayers can

Use digital disclosure service of HMRC as an international disclosure facilityor any other services HMRC provides as a means of correcting their tax non-compliance.

Notify an HMRC's official during the inquiry of the affairs.

Use other methods HMRC is agreed with

Once the taxpayer notifies HMRC about his intention to declare foreign bank accounts within the deadline of 30 September, the tax authorities give 90 days to complete the declaration and pay the tax he/she owes. If the tax affairs of a taxpayer are in order, he/she doesn't need to worry about the penalties.²

However, if someone is unsure, seeking advice from a professional tax attorney is the best way to tackle this.

In case you have an offshore holiday home, it is easier to open a foreign bank account that doesn't pay interest or have a currency account with a local bank in the UK - Wise's Multi-currency account might be able to help you with this. You must retain all the overseas bank statements as HMRC may enquire about your offshore tax position. As HRMC uses CRS information, it is likely to investigate your foreign tax position.

In many cases, HMRC sends letters to taxpayers to confirm that they have declared overseas profits. The letter further includes deceleration for taxpayers to sign and confirm the position. Suppose any asset, regardless of its size or worth, remains undeclared after the deadline. In that case, HMRC enquires into taxpayers' tax affairs and applies a new penalty regime, which may include severe criminal charges.

As mentioned earlier, if you think you own a foreign asset that needs declaration, you may need to take quick actions. Consult a professional whether you have something undeclared from the last ten years or have received a letter from tax authorities.

Maybe you have a foreign bank account in the USA to make payments overseas or maybe because it is easier to transfer payments in your home country with it. Maybe you have bought a rented property in another country to diversify your portfolio.

No matter for what purpose you use your foreign bank account, you must declare it to HMRC. Remember that you're taxable on your worldwide income, profits, and gains as a UK taxpayer, so any interest payment and income you earn from offshore, you should report in the UK to the tax authority.

In this regard, the article explains the importance of declaring foreign bank accounts to HMRC to help you make a timely decision. But it's not meant to give any tax advice and keep in mind that it's better to seek professional advice when it comes to matters that are unclear to you.

**Sources:***Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Black Friday is the day after Thanksgiving, falling on Friday 29th November in 2024. It’s known for being a perfect time for snagging a bargain, opening the...

December kicks off the end of year shopping period, with huge uplifts in on and offline sales as people grab a bargain and get ready for the holiday season....

The term "turnover" is used often in the world of business, but its implications vary significantly depending on the context. At its core, turnover is a...

Wise is a financial technology company focused on global money transfers that offers two different types of accounts: a personal account and a business...

In today's fast-evolving digital landscape, e-commerce is quickly transforming the ways consumers shop and how businesses operate worldwide. DHL’s E-Commerce...

In an increasingly interconnected global economy, small businesses in the United Kingdom (UK) have more opportunities than ever to expand through import and...