Guide on small business payment processing in Australia

Learn how small business payment processing works in Australia, including costs, setup steps, and how to manage domestic and international payments efficiently.

From the supermarket to the servo, we use this domestic-only payment service almost every day. But many Australian business owners still don’t understand what EFTPOS means… or was that eftpos?

Much of the confusion stems from the fact that EFTPOS means different things depending on whether you spell it with upper- or lowercase characters.

In this post, we’re defining EFTPOS/eftpos, discussing the differences, and outlining processes. We’ll also provide relevant info for Australian SMBs, including limitations, fees, and affordable alternatives for offshore payments.

| Table of Contents |

|---|

EFTPOS is a generic term for in-person card payments used worldwide, while eftpos is an Australian domestic-only card with low transaction fees.

EFTPOS stands for Electronic Funds Transfer at Point of Sale. When written in capital letters, EFTPOS is a generic term for a system that facilitates electronic in-person payments, whether by debit card, credit card, or mobile wallet.

The EFTPOS system connects to the customer's account, verifies card details, checks for sufficient funds, and processes the payment. This system is used for in-person card payments worldwide, though sometimes under a different name.

The lowercase “eftpos” is a proprietary brand name for a domestic card scheme used only in Australia. A card scheme is a payment network that defines the standards, security, and fees for branded cards, such as Visa or Mastercard – eftpos is an Australia-only provider.

Take a look at your Australian debit card. Does it have eftpos written on it? Most likely. In Australia, 85%1 of locally issued cards are dual network, using eftpos for domestic payments, and Visa or Mastercard for credit and overseas purchases.

The process to use the low-cost eftpos payment scheme in Australia is as follows:

Tap-and-Go payments follow a similar process, except customers don’t insert a card, select an account, or enter a PIN. The downside is that payments may get routed through international card schemes, which could have higher fees.

While a fraction of a per cent doesn’t look like much, pricier card surcharges can add up over time and impact your bottom line.

Some Australian businesses could reduce expenses through Least-Cost Routing (LCR), which has the POS system automatically selecting the cheapest available payment network. Instead of paying with Visa or Mastercard during Tap-and-Go payments, customers use the cheaper eftpos network.

LCR is usually an opt-in feature. Businesses can try calling their business bank or payment provider to see if it is available. In some situations, activating LCR may require upgrading a POS terminal.

EFTPOS, the all-caps acronym, is a generic worldwide term for in-person card payments of any type. Alternative payment methods include cash, online payment gateways, direct debit, BPAY, Buy Now, Pay Later (BNPL), bank transfers, and payment platforms like PayPal.

The eftpos card scheme differs from its competitors through lower pricing and exclusive domestic use in Australia. When making in-person payments overseas, the cards automatically switch to a global card scheme, such as Visa or Mastercard.

All in-person card payments in Australia use the EFTPOS system. But not all EFTPOS payments use the eftpos-branded card scheme.

Before Tap-and-Go became mainstream, customers would swipe or insert their card in an EFTPOS terminal, select a “SAV” or “CHQ” account, and enter their PIN to pay with the low-fee eftpos card scheme.

Nowadays, most Aussies make contactless payments with a card or mobile wallet, which lets the terminal automatically select a payment network. Sadly, more often than not, the terminal shuns the low-cost eftpos card scheme in favour of pricer, more lucrative Visa or Mastercard networks.

Consumers can usually pay with the cheaper eftpos scheme by inserting their card instead of tapping. While this saves on processing fees, many people, including some high-volume businesses, find it too time-consuming and inconvenient.

In Australia, EFTPOS fees vary depending on the card scheme, business size, and payment processor (Square, Stripe, etc.). Some businesses pay a flat-rate fee, such as 0.30c per transaction, while others pay a percentage-based fee, or a mix of the two.

According to the Reserve Bank of Australia, card scheme fees have an average total transactional value of:

In Australia, 16% of businesses pass card fees onto customers through a POS surcharge at checkout.3 That’s why when you purchase a $5 coffee, for example, you may end up paying 1-2% more, either through a flat fee or a percentage-based surcharge.

If your business has card surcharges, the Australian Competition & Consumer Commission (ACCC) requires that you don’t charge more than what it costs you. You must also be able to prove those costs if asked.

If there is no way for a customer to avoid surcharges, the ACCC also requires that you include all surcharges within the display price.4

The Reserve Bank of Australia will ban card surcharging on October 01, 2026. From that date, businesses can only charge customers the listed price, regardless of how they pay. Surcharges for Visa, Mastercard, eftpos or any other payment network will no longer be allowed.

In good news for businesses, the Reserve Bank plans to lower the caps on interchange fees, which it expects to reduce payment costs.5 The upcoming change should also improve fee transparency, making it easier for businesses to shop around.

Despite the fees, the in-person EFTPOS card payment system has many benefits for businesses.

The low-cost eftpos card scheme also offers numerous benefits.

While in-person EFTPOS payments – and the eftpos card scheme – offer a plethora of benefits, there are downsides to consider.

Despite the drawbacks, most Australian SMBs accept EFTPOS payments, as few in-person customers are willing to pay in cash.

While optimizing your domestic EFTPOS setups can help manage local card transaction costs, local solutions fall short when your business operations cross borders. For Australian businesses managing international suppliers, remote teams, or global customers.

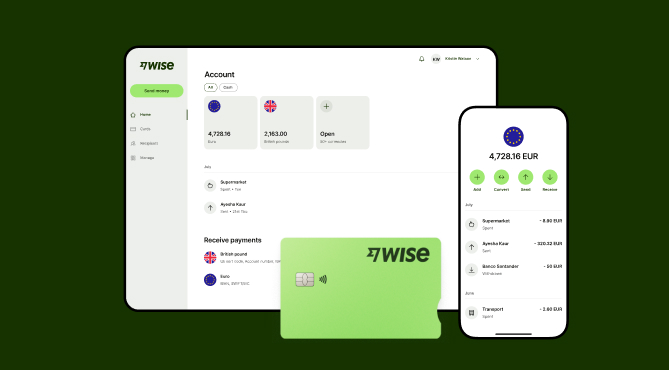

Expanding a business globally opens up exciting opportunities, but also new challenges like receiving payments across borders. Hidden foreign transaction fees and hefty currency conversions involved with international payments can eat into your profits and time.

Wise Business serves as a cost-effective solution where you can receive money from around the world at the speed and price of local payments.

Transform the way you receive payments with Wise Business:

Sign up for the Wise Business account! 🚀

This general advice does not take into account your objectives, financial circumstances or needs and you should consider if it is appropriate for you.

Sources:

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Learn how small business payment processing works in Australia, including costs, setup steps, and how to manage domestic and international payments efficiently.

Not sure what a merchant account is? No worries. From definitions to benefits, requirements, and setups, we’re covering everything the Aussie SMB should know.

Learn how secure online payments work in Australia, the safest methods for businesses, and how to protect customer transactions and international payments.

Learn what integrated payments are, how they work, and how to set up a system. A practical guide for Australian businesses looking to simplify payments.

Learn how electronic funds transfers work, domestic vs international requirements, processing times, and the different types of EFTs for Australian businesses.

Compare Adyen vs Stripe for Australian businesses. Explore features, fees, and how Wise Business can reduce international payment costs.