Guide on small business payment processing in Australia

Learn how small business payment processing works in Australia, including costs, setup steps, and how to manage domestic and international payments efficiently.

Online payments are a part of everyday business in Australia, with customers regularly making purchases through ecommerce stores or transferring money internationally. But as cyber threats like phishing scams and payment fraud rise, fully securing these payments has become a top priority.

The guide explains what secure payments are and why they matter, and the practical steps businesses can take to protect transactions, especially when moving money across borders – a process that Wise Business can help with.

| Table of Contents |

|---|

A secure payment is a transaction designed to protect money and sensitive financial information (e.g. card details, bank account info) from being intercepted and misused. To achieve this, secure payment systems use a variety of cutting-edge technologies and processes, such as gateways and encryption.

For businesses, secure online payments rely on this tech and systems working together behind the scenes:

In Australia, businesses taking card payments are generally expected to comply with PCI DSS (Payment Card Industry Data Security Standard). This is a global framework that helps businesses protect cardholder data and reduce the risk of cyber incidents, such as data breaches and fraud.

However, problems with unsafe payments persist for both customers and businesses. A study by the National Anti-Scam Centre found Australians lost $260+ million in online shopping scams in 2025¹. Similarly, micro and small enterprises in Australia lost $152.6m to payment redirection scams in 2024².

PCI Security Standards outlines six main ‘threats’ businesses should be aware of³:

As more Australian businesses rely on ecommerce for sales, as well as on digital invoicing and international transactions across both B2C and B2B settings, the importance of secure payment systems has risen in tandem. They play a huge role in protecting both your revenue and your customer-client relationships.

There are numerous safe methods Australian businesses can use to take online payments, many with security features built in to protect customers.

These include:

Securing online payments requires a collection of policies and tech that work together to create a system that protects your business and your customers. It’s not a ‘one and done’ process either – you’ll need to manage and refine everything over time.

This is the best place to start. Any Australian business that takes cards and stores payment details must comply with PCI DSS, which isn’t a law, but a security standard with things you have to do to remain compliant⁵.

These requirements include⁵:

You’ll also have to make sure any third-party you work with meets PCI DSS requirements, too, such as a payment processor or gateway, so always keep this in mind. A compliant provider will have systems in place that protect cardholder data and reduce risks (fraud, breaches, etc.)

Customers expect to see secure web pages when they navigate to a site, especially checkouts. They’ll usually scan for a ‘padlock icon’ to the left of the address bar and make sure the URL begins with HTTPS.

A secure website should always:

Weak passwords are a big vulnerability, so it’s vital to add an extra verification step to your business payment systems, admin accounts, and backend website logins through multi-factor authentication (MFA). This includes processes like SMS verification codes and one-time login approvals, which reduce the chances of ‘unauthorised access’.

And always remember to keep software and plugins updated as well, as outdated systems create security gaps cybercriminals can exploit.

This is an important one, as most small businesses need a payment gateway to facilitate transactions, acting as an intermediary between a website or POS and banks. Reputable providers typically include quite a few security-related features, including encryption, fraud screening, and compliance support

Also, this is where you’ll want support for the secure online payments outlined earlier, and to make sure there are clear refund and dispute processes. You should communicate these clearly to customers to increase transparency and trust.

Securing your checkout experience is also essential. Customers should only enter details through secure, verified checkout pages or payment links. Avoid manually sending bank details via email or SMS, as this increases the risk of scams and fraud. Trusted payment providers usually offer encrypted, secure checkout systems by default.

Systems are good, but you need oversight. Many payment breaches happen because something suspicious goes unnoticed. You should monitor for unusual payment behaviour. Keep an eye out for:

Most payment providers include fraud monitoring tools to flag ‘shady’ activity, but it’s also useful to train staff to spot phishing emails, fake invoices, and other scams, especially if they regularly handle online payments or data.

The government has a 6-step guide for protecting customer information, which is an extension of the Privacy Act 1988. Part of this is either ‘destroying’ or ‘de-identifying’ any sensitive information when you no longer need it⁶.

This is common sense, too: the less data you have stored on your systems, the less likely you are to be affected by a breach. Many payment providers now use tokenisation systems that obscure card details with digital tokens to help with this.

International payments can introduce additional security concerns compared to domestic transactions, as they involve more ‘variables’ – multiple banks, currencies, regulations, etc.

Customers and businesses may think twice about sending money overseas, especially large sums, because of concerns about:

Because international payments involve more moving parts, there’s a need for extra visibility and protection when sending money overseas.

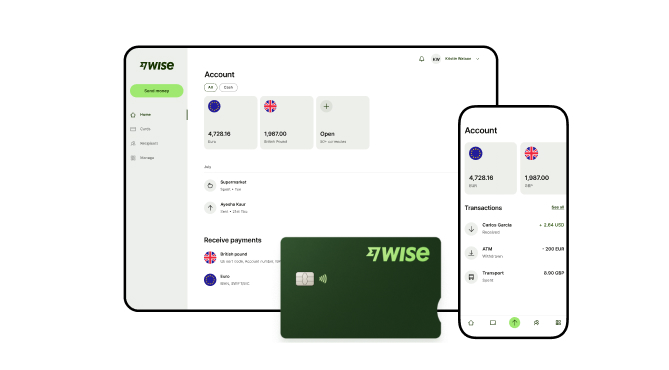

Wise Business has security built into its platform for businesses that require a super-safe system for cross-border transactions. Features include 2FA to verify it’s really you making payments, biometric login and encryption through the Wise app, plus customisable controls like auto log-out and permission settings.

A Wise Business account allows users to can send, receive, and hold in multiple currencies. Experience hassle-free global transactions by transacting like a local business. Here's what you get with a Wise Business account:

Sign up for the Wise Business account! 🚀

This general advice does not take into account your objectives, financial circumstances or needs and you should consider if it is appropriate for you.

**Capital at risk, growth not guaranteed. Interest is the name of a custody and nominee service provided by Wise Australia Investments Pty Ltd in partnership with Franklin Templeton.

Sources:

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Learn how small business payment processing works in Australia, including costs, setup steps, and how to manage domestic and international payments efficiently.

Not sure what a merchant account is? No worries. From definitions to benefits, requirements, and setups, we’re covering everything the Aussie SMB should know.

Learn what integrated payments are, how they work, and how to set up a system. A practical guide for Australian businesses looking to simplify payments.

From payment networks to processes, we’re detailing what EFTPOS means and how it differs from the Australian domestic-only eftpos card scheme.

Learn how electronic funds transfers work, domestic vs international requirements, processing times, and the different types of EFTs for Australian businesses.

Compare Adyen vs Stripe for Australian businesses. Explore features, fees, and how Wise Business can reduce international payment costs.