How to Expand Your Business Internationally: A US Guide

Discover actionable steps for US businesses to expand internationally; research markets, plan effectively, and manage finances to achieve global growth.

Cash flow management is one of the biggest challenges US businesses face. Delays in vendor payments, limited options for sending money, and high transaction fees can quickly impact operations. To address these issues, many companies are turning to modern payment platforms such as Plastiq and Melio.

Both services aim to make business payments easier, but they approach the problem in different ways. Plastiq focuses on flexibility by enabling credit card payments to almost any vendor, while Melio emphasizes cost savings through free bank transfers and automated accounts payable. Learn how these differences play out in practice so you can decide which platform best supports your business. We'll also discuss the Wise Business account. The global account that can help your company with all things cross-border.

Do you send and receive global payments?

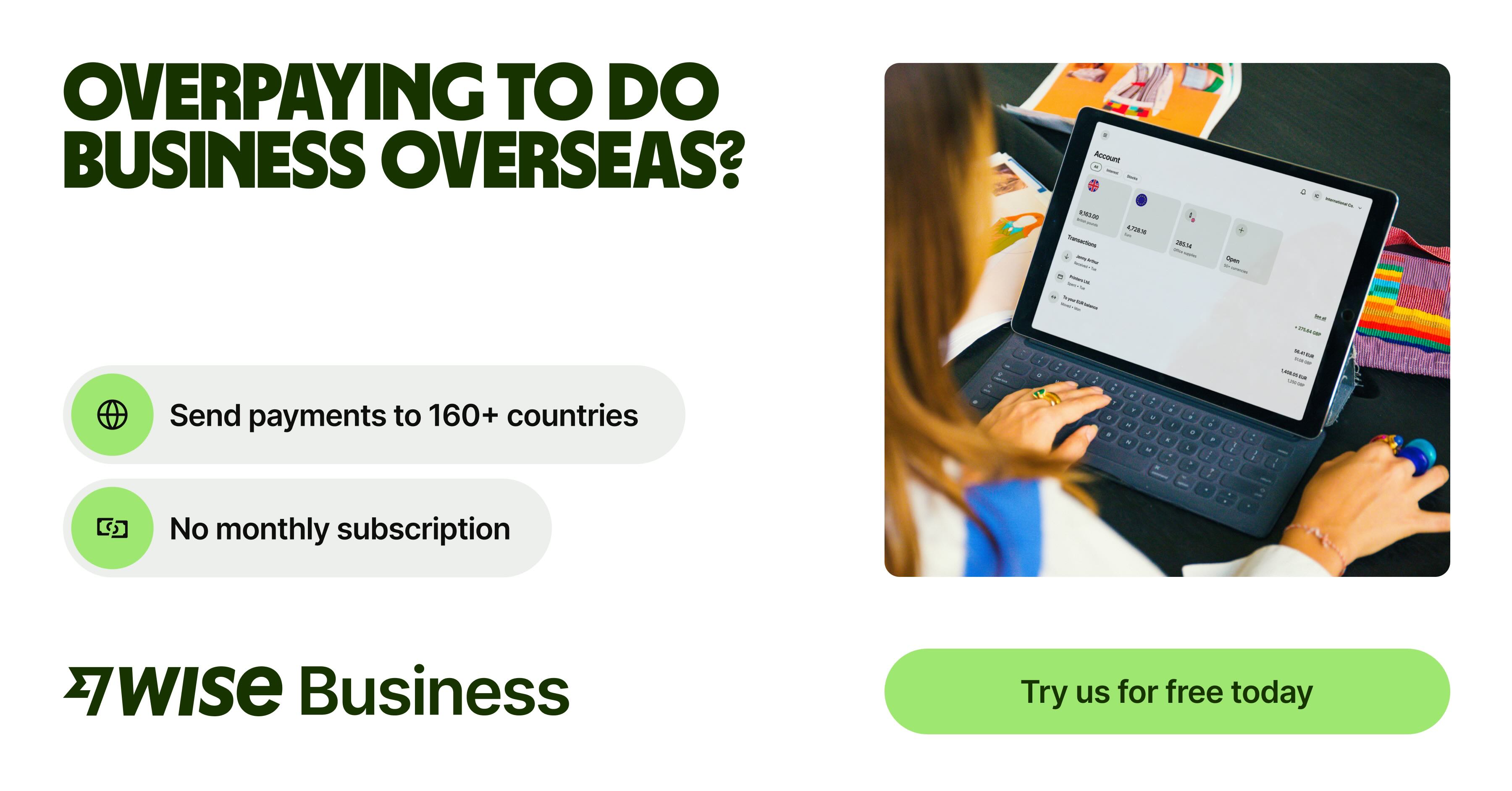

Wise Trustpilot Score: 4.3 stars on 230,000+ reviews

No minimum balance requirement and no monthly fees

Integrates with QuickBooks, Xero, Sage, and more

Plastiq is a payment platform designed to give US businesses maximum flexibility. Its core feature is allowing companies to pay vendors by credit card, even if those vendors don’t normally accept card payments. Plastiq charges your card, then pays the vendor through ACH (Automated Clearing House), wire transfer, or check.1

This model provides two major benefits for American business owners. First, it extends cash flow by letting them use credit lines to cover operational expenses. Second, it enables them to collect valuable credit card rewards on payments that would otherwise require bank transfers.

Plastiq also supports international transactions in more than 45 countries, making it useful for US firms with overseas suppliers.2 While accounting integrations are limited, Plastiq’s focus on vendor flexibility makes it appealing to companies that prioritize credit leverage.

Melio was built with small US businesses in mind. Unlike Plastiq, it emphasizes free, simple bank transfers. Business owners can pay vendors directly via ACH for a $0.50 fee or use a credit card for a 2.9% fee.3

One of Melio’s biggest strengths is integration with accounting tools. QuickBooks and Xero users can sync their accounts payable directly, saving time and reducing bookkeeping errors.

While Melio does allow credit card payments, it is not as flexible as Plastiq when dealing with vendors that don’t typically accept them. Instead, its competitive edge lies in cost savings and automation. For US companies paying mostly domestic suppliers, Melio offers a streamlined experience that fits directly into existing workflows.

Wise is not a bank, but a Money Services Business (MSB) provider and a smart alternative to banks. Wise makes it easy to send, hold, and manage business funds in 40+ currencies. You can get major currency account details for a one-off fee to receive overseas payments like a local. Simply add the local account details when billing international customers to receive international payments with no fees.

Account opening is 100% online, with no need to visit a branch or book appointments.

Once you’re set up, you can connect to software such as Wave, FreshBooks, and more. You can also withdraw funds from Stripe without currency conversion fees.

Open a Wise Business account online

| Some key benefits of Wise Business include: |

|---|

|

| Payment Type | Plastiq5 | Melio3 |

|---|---|---|

| Credit card | 2.9% | 2.9% |

| ACH bank transfer | $0.99 | $0.50 |

| International payments | $39 | $20 (ACH) \ 2.9% + $20 (Card) |

| Check delivery | $1.49 | $1.5 |

Melio is cheaper for ACH and international transfers, while credit card and check fees are nearly identical.

Plastiq’s global reach is one of its defining features. With the ability to send funds to more than 45 countries, it’s attractive to US businesses managing international supply chains. Vendors can receive money in local currency, often through wire transfers.

Melio does support international payments, but its network is more limited and processing times are slower. Extra bank fees may also apply. For US entrepreneurs working primarily with domestic vendors, this is not an issue. But for companies importing goods or paying contractors abroad, Plastiq holds the edge.

Plastiq functions primarily as a payments processor, with fewer integrations into accounting systems. While you can export data, it doesn’t offer the same level of automation as its competitor.

Melio, on the other hand, was built with accounting in mind. Its deep integration with QuickBooks and Xero makes it easy to reconcile payments, manage invoices, and stay compliant. For US small businesses that handle many recurring bills, Melio’s automation reduces admin time and helps avoid late fees.

Both Plastiq and Melio maintain high compliance standards to safeguard business transactions.

Plastiq has been PCI DSS Level 1 certified since 2015, the highest standard for handling card payments. It uses bank-grade security and military-grade encryption, combined with tokenization to protect sensitive financial data. Plastiq also employs advanced risk analysis to identify potential fraud and ensure that payments remain secure. The platform is SOC 2 Type II certified, which demonstrates strong controls for data security and privacy.6

Melio emphasizes compliance with international frameworks to protect customer information. It is also SOC 2 Type II certified, and holds multiple ISO certifications, including ISO/IEC 27001:2022 for information security management, ISO/IEC 27017:2015 for cloud security, and ISO/IEC 27018:2019 for cloud privacy. These certifications reflect Melio’s commitment to safeguarding data across its cloud-based platform.7

For US businesses, both providers deliver enterprise-grade protections.

When comparing Plastiq vs. Melio, the better choice depends on your priorities as a US business owner.

Plastiq is the stronger option if you want maximum flexibility. Its ability to convert credit card payments into checks, wires or ACH transfers makes it useful for paying almost any vendor, whether domestic or international. For companies that rely on credit lines to extend cash flow or want to capture credit card rewards on everyday expenses, Plastiq provides a clear advantage.

Melio stands out for cost efficiency and ease of use. With free or very low-cost ACH transfers and deep QuickBooks and Xero integrations, it reduces payment overhead and simplifies bookkeeping. For small businesses with mostly US-based suppliers, Melio delivers a streamlined, affordable way to manage accounts payable.

Plastiq fits businesses that value payment flexibility and global reach, while Melio is better suited to firms focused on cost savings and automation. The right platform is the one that aligns most closely with your operating model and growth goals.

Not usually. Melio offers ACH transfers at a fixed $0.50 rate, while Plastiq charges for most card-based payments.

Melio has stronger integration with QuickBooks and Xero, making it easier for small businesses.

Yes, but coverage is limited and processing is slower than Plastiq.

Yes. Even if vendors don’t accept cards, Plastiq routes the payment as ACH, check, or wire.

| Looking for more Melio Comparisons? |

|---|

| Melio vs. QuickBooks |

| Melio vs. Bill.com |

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Discover actionable steps for US businesses to expand internationally; research markets, plan effectively, and manage finances to achieve global growth.

Looking for a Philippines Business Visa? Our guide for US citizens covers requirements, fees, and processing steps for a smooth trip.

Learn how to register a US business in Australia. Navigate legal requirements, foreign company registration with ASIC, and the Australian tax system.

Understand Australia's corporate tax rates for 2025-26: a base rate of 25% for small businesses and a standard 30% for all other entities.

Learn how to register a business in India from the US. Our guide details steps, documents, and key financial considerations for aspiring entrepreneurs.

Learn how to get your India business visa. A step-by-step guide for US professionals on requirements, applications, and costs.