Chase foreign transaction fees: Complete guide

Everything you need to know about Chase foreign transaction fees.

If you're a frequent visitor to Switzerland, or you’re planning to move there, you may be wondering about how to open a bank account in Switzerland.

This guide to opening a bank account in Switzerland covers all you need to know, including the documents needed, the options for online and remote account opening, and some popular Swiss banks to consider.

We’ll also touch on a banking alternative where you can hold CHF before you move — from Wise.

There’s no legal reason why a US citizen can’t open a bank account in Switzerland. However, there may be some banks which do not offer services to US citizens and US related persons.

Other banks may require extra checks to open your account, or may not offer online account opening for example.

The US Embassy in Switzerland¹ recommends trying major banks at their regional centers in Geneva, Bern, Basel or Zurich, as these branches may be able to offer a broader range of support to US citizens.

It is possible to open a bank account in Switzerland remotely, although not all banks offer all products for online and in-app opening.

You’ll also need to fit certain eligibility criteria. For example, to open an account with Post Finance®, through their app, you must be a new customer aged over 18 and a legal resident of Switzerland already².

If you fulfill these criteria, you can apply for your account in the app, and then you’ll verify your identity through a video call. However, the video verification process can take up to 7 days to complete, so this isn’t necessarily an instant process.

Other banks may not accept US ID for online account opening. This is the case for the UBS® Key4 banking package³, as an example.

| If you’re looking for an account you can use to hold CHF before you move to Switzerland you may be better off with an alternative — we’ll cover the Wise Account which you can open before you move, to hold and exchange both USD and CHF, later. |

|---|

Expect to be asked to show your ID, residence and address documentation when opening an account in Switzerland.

| The documents required will vary between banks, but will likely include: |

|---|

|

If you are not yet resident in Switzerland you may still be able to open a non-resident account with a Swiss bank — but the terms and conditions, as well as the fees you pay, may not be the same as the typical accounts offered to Swiss legal residents.

When you open a bank account you are likely to be assigned an individual account manager. If you need to communicate in English, let your bank know in advance to ensure they can assign you an English speaking contact.

Otherwise you will be assigned a contact who speaks one of the four official languages of Switzerland. Get the direct contact details of your account manager as soon as you can, to make corresponding easier.

Because many people live in Switzerland but work elsewhere in the surrounding Eurozone (or vice versa), many banks offer accounts which allow withdrawals in both Swiss francs and euros. This can be a helpful perk if you are one of the many cross border commuters in the area. See what options your chosen bank can offer.

There’s usually an opening minimum balance you’ll need to deposit right away to get your Swiss bank account set up.

Then, everyday bank accounts in Switzerland incur fees, including common costs like a monthly maintenance charge, out of network ATM fees and transfer fees.

There are also fees to get a credit card, and many accounts charge more if you’d prefer to receive paper statements.

Because of the range of additional fees and charges, it is worth looking at the details for each account carefully before choosing the product that works best for you.

In some cases you might get fees reduced or waived if you have savings with the same bank, or take a mortgage with them. Ask your account manager what they can offer you before you decide.

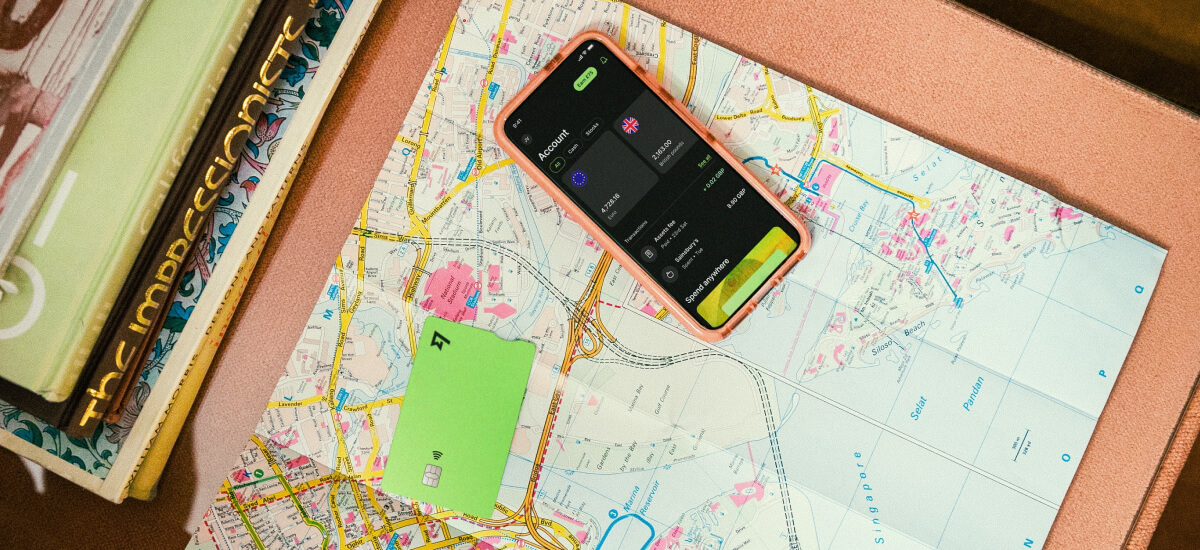

If you’re looking for an alternative to banking to hold, exchange, send and spend CHF, before you’ve even moved to Switzerland, you need the Wise Account.

Open your Wise account online or in the Wise app, to manage a balance in 40+ currencies including CHF and USD, and to get a linked Wise Multi-Currency Card you can use for spending in 170+ countries.

You’ll be able to add funds in USD and switch over to CHF or the currency of your choice with the mid-market rate and low fees from 0.41%⁴, to make it easier and cheaper to manage your life in a new country.

Please see Terms of Use for your region or visit Wise Fees & Pricing for the most up to date pricing and fee information

It can seem like there are an overwhelming number of choices when it comes to Swiss banks. Here are a few major Swiss banks you might consider for your CHF everyday account:

Once you're set up, banking in Switzerland will quickly become familiar. Many large banks have details online in English, and are likely to be able to assign you an English speaking account manager if your Romansh (or French, German or Italian) is a little rusty.

With online banking as the norm, you can manage most of your transactions easily that way, and focus on daily life.

Check out the banks we’ve looked at here, and compare them against the flexible Wise Account to pick the one that suits you best.

Sources checked on 05.26.2023

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Everything you need to know about Chase foreign transaction fees.

Everything you need to know about PNC credit and debit card foreign transaction fees.

Wondering how to open a foreign currency account in the US? Struggling to find information? Read on to find out what you need.

Considering closing your foreign bank account? Discover the tax implications, benefits, and steps involved in making this decision. Learn more here.

Learn how to close your ADCB account from abroad with this comprehensive guide. Discover the steps, required documents, and tips for a smooth process.

Learn how to close your UAE bank account from abroad with this comprehensive guide. Discover the steps, required documents, and tips for a smooth process.