How to Open a Freelancer USD Account in the Philippines with Wise

Are you a Filipino freelancer? Learn how to get your own US/Euro account details. Receive USD, convert to PHP at the real rate, and save on fees

Being a freelancer in the Philippines offers freedom and flexibility, but it also comes with challenges, like securing healthcare without a corporate plan. Thankfully, health maintenance organizations (HMOs) provide insurance plans that can protect you from costly medical emergencies.

This article will explain what an HMO is, what it covers, why it’s essential for freelancers, what to look for in a plan, and how to avail an HMO for self-employed workers. We'll also introduce the Wise account, a handy companion to make your money go further with low, transparent fees.

| Table of contents |

|---|

✍️ Sign up for a free account now

HMOs offer health insurance coverage that provides comprehensive medical services through a network of accredited doctors, clinics, and hospitals. Members pay a fixed monthly or yearly premium and can access covered healthcare services, usually with minimal out-of-pocket costs, as long as they use providers within the HMO network.

Every HMO plan is different, but most cover¹:

Medical emergencies in the Philippines can be costly. A single hospitalization can range from tens of thousands to hundreds of thousands of pesos, particularly if specialized care or surgery is needed.²

Choosing the best HMO for freelancers ensures you have a safety net that protects your finances and health.

If you’re wondering what is the best HMO in the Philippines, there’s not one definite answer. It depends on your needs and budget, but here are some features to compare when choosing an HMO.

Consider your healthcare needs and determine whether the HMO plan suits them. For example, if you attend therapy or counseling, you may want to find a plan that covers mental health services.

And, if you have a pre-existing condition, you’ll likely want coverage for it. Unfortunately, most HMOs impose a waiting period of 1 to 2 years before your pre-existing condition is covered.³ You may also have to pay a higher premium for this coverage. If you do have a pre-existing condition, make sure you read each HMO’s policy carefully to determine what coverage you’d get for it and when.

The top HMOs in the Philippines all have their own network of accredited hospitals and clinics. Try to find an HMO that works with facilities near your home or work. Otherwise, you may have to go to and pay for an out-of-network facility in an emergency.

The annual benefit limit is the maximum amount the HMO will pay per year. If you exceed the ABL, you’ll have to cover the extra costs yourself. The best HMO for freelancers typically offers higher limits for more comprehensive protection.

Costs vary depending on coverage, age, and provider. You can typically request a free quote with your particulars to make an informed decision.

Be sure to look at the different payment options as well, as monthly, quarterly, and annual payment plans are all common.

Many of the best HMOs for freelancers offer teleconsultation, online appointments, and remote monitoring. This is especially useful for freelancers with irregular schedules or those who live far from healthcare facilities.

If you’re wondering how to avail an HMO for self-employed workers, the process is simple. Here’s a step-by-step guide to help you secure the best HMO for freelancers.

Before you can choose an HMO, you need to assess your personal healthcare needs and budget. Consider how frequently you visit doctors, whether you need coverage for dependents, and how much you’re willing to pay for a plan on a monthly, quarterly, or annual basis.

If you’re not sure how much coverage you’ll need, some HMOs let you upgrade to a higher tier mid-year so you don’t have to pay out-of-pocket for additional healthcare services.

Now that you have a clear idea of your needs, you can start researching and comparing different HMO providers. Here are some of the top HMOs in the Philippines:

To choose an HMO, look into what their plans cover, their network of accredited hospitals and clinics, their Annual Benefit Limit, and the cost of each plan.

Consider reading online reviews for each provider as well to identify the best HMO for freelancers.

HMOs typically offer multiple insurance plans with different coverage, so ensure you peruse them all before looking into another HMO.

Once you’ve chosen an HMO, you can apply for your plan online or in person if there’s a branch near you. Make sure you have the necessary documents for a smooth application process. You may need:

If you have pre-existing conditions, HMOs may request medical records or a physical examination as well before approving you.

After collecting all the required documents, submit your application to your chosen HMO. Once your application is approved, you can pay for your plan using a credit card, bank transfer, or online payment.

You’ll then receive a membership card or digital ID, giving you access to the HMO’s services at its network of healthcare institutions. Take time to familiarize yourself with the covered services, accredited facilities, and the process for claims and reimbursements to ensure you’re getting the most out of your plan.

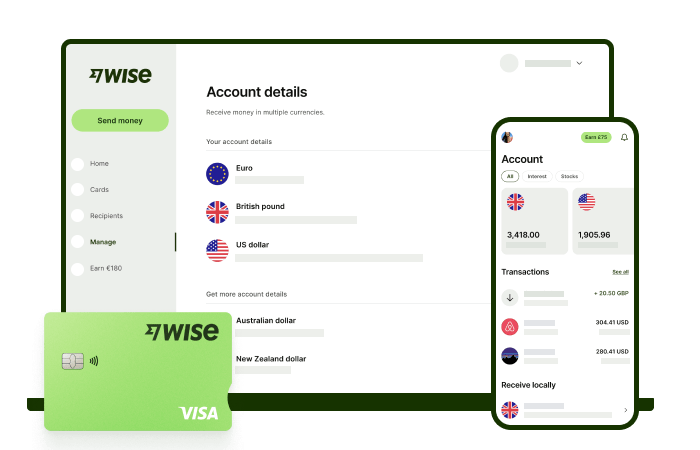

Did you know that over 76%* of Filipinos cite low and transparent fees as an important factor when receiving money from abroad? With Wise, that's exactly what you're getting - all you need to get started is to sign up for a free Wise account, and you'll be able to manage your money with just a few taps of your phone.

You'll have access to 8+ local account details for major currencies including PHP, USD, GBP, AUD, and more, allowing you to receive money directly, in a cheap and convenient manner. After getting your money, you can easily convert it to 40+ currencies, with low fees, and the mid-market rate - also known as the rate you see on Google. This includes exchanging to PHP with a one-time conversion fee from 0.57% that's shown upfront, and no markups or additional fees.

Get paid and move your funds to your local bank account in PHP in a cheap and convenient manner with Wise to stretch every peso.

*Disclaimer: The percentage figure mentioned above is based on an internal survey conducted by Wise in April, 2024

✍️ Sign up for a free account now

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Are you a Filipino freelancer? Learn how to get your own US/Euro account details. Receive USD, convert to PHP at the real rate, and save on fees

Learn how to get a BIR Certificate of Registration (Form 2303) in 2026, including requirements, steps, and how to apply online.

Searching for the best laptop for a virtual assistants? Our guide covers top specs, brands, and budget options to boost your WFH productivity.

Ready for a non-voice WFH job? This guide covers roles (with salaries!), essential skills, where to find legitimate postings, and how to get paid.

Explore the types of virtual assistant work. Find your niche, from social media to data entry, and learn how to manage client payments easily.

Your guide to landing direct client virtual assistant jobs from the Philippines. Learn where to find clients, build your portfolio, and get paid easily.