How to Expand Your Business Internationally: A US Guide

Discover actionable steps for US businesses to expand internationally; research markets, plan effectively, and manage finances to achieve global growth.

How much time does your small business spend manually processing payments each month? What does it cost to process each payment? Business-to-business (B2B) payment automation, which many companies are already embracing, could be the key to helping you save time and money.

And yet, a significant number of businesses continue with manual processes and the difficulties they introduce. In fact, according to PYMNTS, only 5% of mid-sized firms have fully completed the automation of all AP and AR processes.1

Unfortunately, a lack of automation can come at a high price for businesses. According to the Institute of Finance & Management, manually processing a single invoice costs a business up to $16. But automating this process can reduce the cost to as little as $3.2

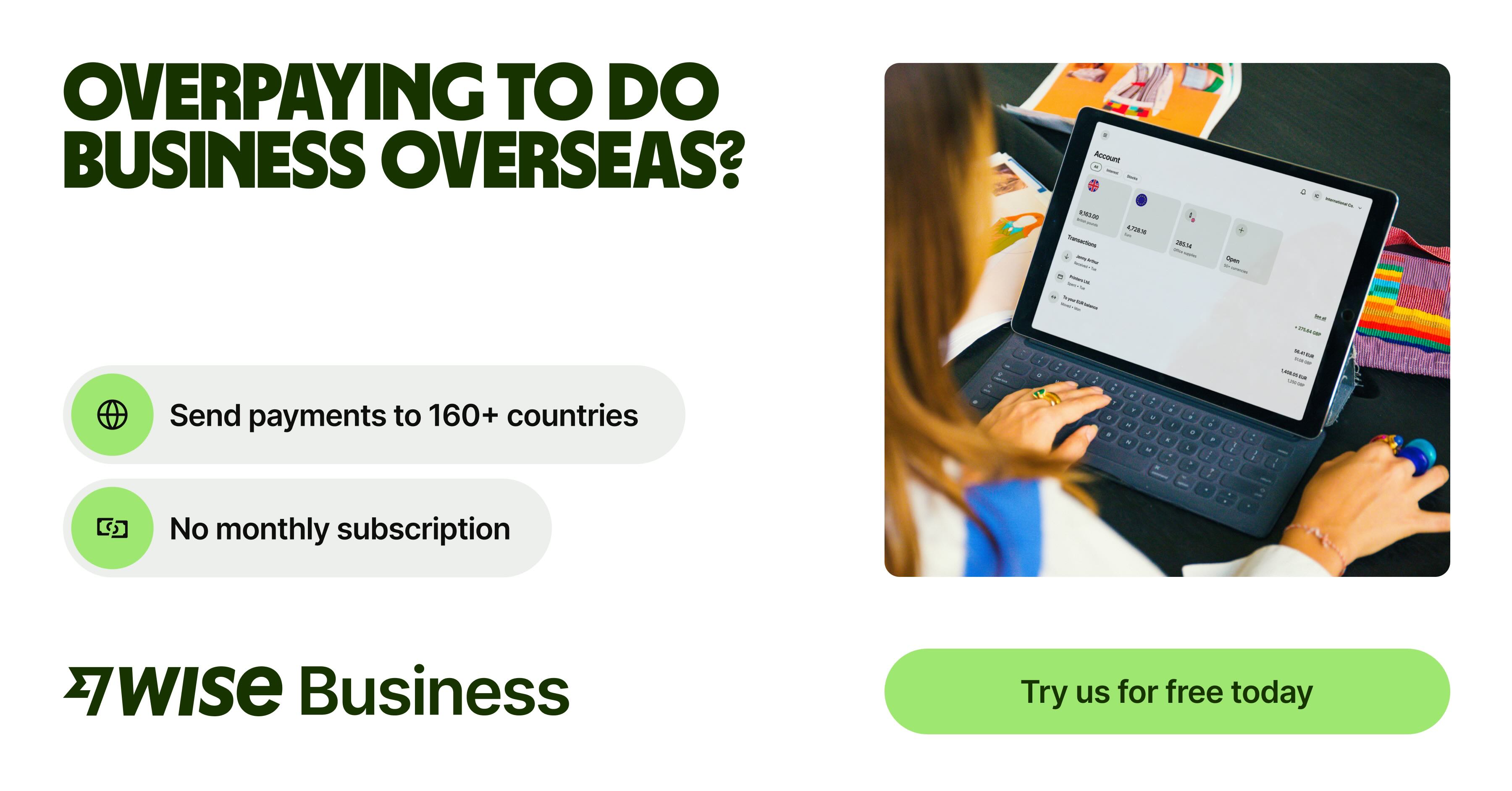

Beyond cost savings, automation means fewer human errors, faster transactions and better fraud prevention. This article will explain what B2B payment automation is, why it’s valuable for a growing business and how you can start to automate B2B payments in your own company. We'll also discuss the Wise Business account. The global account that can help your company with all things cross-border.

Do you send and receive global payments?

Wise Trustpilot Score: 4.3 stars on 230,000+ reviews

No minimum balance requirement and no monthly fees

Integrates with QuickBooks, Xero, Sage, and more

B2B payment automation is the process of using software and digital systems to handle business-to-business payments without manual effort.

Automating how your company pays vendors and receives payments from clients usually means moving away from paper checks, emails and spreadsheets. Instead, you use an electronic platform that manages the entire payment workflow, including invoice receipt, approval, payment execution and reconciliation.

Rather than your AP clerk printing checks or entering bank transfers by hand, an automated system can, for example, automatically schedule an Automated Clearing House (ACH) transfer to a vendor on the due date and record the transaction in your accounting software.

Automated B2B payments often integrate with your accounting or Enterprise Resource Planning (ERP) system. This way, invoices are captured digitally, approvals can happen online and payments are sent electronically through methods like ACH, wire or virtual card. The system can then mark the invoice as paid and update your ledgers, all with minimal human intervention.

Importantly, B2B payment automation is not just for major enterprises. Today, there are many cloud-based solutions that a 10- or 15-person company can use to automate payments without a big IT project.

Whether through your bank’s online bill pay, a dedicated accounts payable automation tool or a service for international payments, even small businesses can set up B2B payments automation to streamline their finances.

Automation might sound like a big step, but it brings tangible benefits that directly impact your business’s bottom line.

| Here are some of the main advantages of B2B payment optimization through automation: |

|---|

| Efficiency: Automating payments drastically cuts the time spent on each transaction. There’s no need to manually write checks, enter data or chase approvals. This means your finance team can handle a higher volume of payments with less effort. Just imagine the time your team will save when they don’t need to micromanage each invoice! |

| Lower Costs: Automation diminishes both labor and processing costs. Traditional payments involve expenses like check stock, postage, bank fees and error correction. Automated payments cost less per transaction, and the savings can boost your margins. |

| Fewer Errors and Improved Accuracy: Manual processes often lead to mistakes, like entering the wrong amount or paying the wrong vendor. Automation reduces those risks by applying consistent tests, such as instantly matching invoices to purchase orders and flagging any issues. |

| Better Cash Flow Management: Automated payments give you better control and visibility over cash flow. You can schedule them to optimize timing, and dashboards help you track upcoming payments and plan accordingly. Not to mention, one study found that manual payment processes require 67% more time for follow-up on overdue payments.3 |

| Security and Fraud Prevention: Paper checks and manual processes are slow and less secure. Electronic payments reduce risks with features like encryption, two-factor authentication and audit trails. These are just a few reasons why many companies are shifting away from checks. |

| Enhanced Supplier and Client Relationships: Faster, more reliable payments mean happier business partners. When your system pays vendors on time (or even early), you build trust and credibility. Automation can ensure no invoice falls through the cracks, so you won’t inadvertently strain a relationship by paying late. Some automated AP platforms even let suppliers track payment status in real time, reducing the number of “Have you paid this invoice yet?” phone calls. |

| Real-Time Insights and Audit Trail: With transactions digitized, you get instant visibility into your finances. You can generate reports on how much you spent by vendor, how long payments take and where the bottlenecks are occuring. This data helps in negotiating better terms with suppliers or identifying inefficiencies. |

[](https://wise.com/us/business/)

Next, we’ll look at how businesses actually make payments, whether manual or automated, and which methods are most popular today.

Paper checks might have once been king, but now, businesses have all kinds of B2B payment methods at their disposal:

The best option for your business will depend on a lot of things, but electronic options are clearly gaining momentum, largely thanks to the benefits of payment automation.

In the next section, we’ll discuss how you can start automating your payment process.

Here’s a simple roadmap to get started with B2B payments automation:

Keep in mind that you don’t have to achieve 100% automation overnight. You can start with partial automation (maybe just the payment execution while still doing approvals manually), and then gradually automate more pieces as you get more comfortable with it.

What matters is that you’re taking the first step away from purely manual payments, and once you do, the advantages will become evident quickly.

| Use Auto-Conversion for International Payments |

|---|

| Keep an eye on exchange rate trends and consider using the auto conversion tool in your Wise Business account, so you never miss out on a favorable exchange rate. This can help mitigate risks associated with currency fluctuations and maximise your cash flow. |

Automate Your Currency Conversions >>

B2B payment methods are the ways in which businesses pay each other for goods and services. This term doesn’t refer to one single method, but rather encompasses all the common payment options used in business-to-business transactions.

Classic B2B payment methods included paper checks and cash; however, most B2B payments now occur through electronic methods.

The leading B2B payment methods are:

In terms of speed, cost and convenience, each option has its pros and cons. For example, ACH transfers are relatively cheap, but they’re not instantaneous. On the other hand, wire transfers are same-day, but come with higher fees.

Businesses choose the method that best fits the transaction, accounting for factors like the amount, the urgency and whether they’re paying someone overseas or domestically.

In recent years, many companies have been shifting from the old methods (especially paper checks) to digital methods. Much of what is driving this shift is the need for faster processing, better tracking and lower risk of fraud.

So, if someone asks what the B2B payment method is, they’re likely referring to the array of payment options businesses use, with an understanding that electronic payments (ACH, wires, etc.) are now the primary methods in use.

The most popular B2B payment methods today are primarily electronic.

They include:

Not to be overlooked, some businesses still use paper checks, especially in the U.S. However, in some countries, including China, Japan and South Korea, checks are almost non-existent for payments now.

Finally, online payment platforms have gained popularity for certain scenarios, such as paying a freelance contractor overseas or handling marketplace transactions. Real-time payments are also on the horizon as a popular method, although their adoption is only just gaining momentum.

It generally only entails a few quick steps to make a B2B payment, but the exact process will depend on the method of payment you choose.

Here’s a quick overview of how to make a B2B payment:

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Discover actionable steps for US businesses to expand internationally; research markets, plan effectively, and manage finances to achieve global growth.

Looking for a Philippines Business Visa? Our guide for US citizens covers requirements, fees, and processing steps for a smooth trip.

Learn how to register a US business in Australia. Navigate legal requirements, foreign company registration with ASIC, and the Australian tax system.

Understand Australia's corporate tax rates for 2025-26: a base rate of 25% for small businesses and a standard 30% for all other entities.

Learn how to register a business in India from the US. Our guide details steps, documents, and key financial considerations for aspiring entrepreneurs.

Learn how to get your India business visa. A step-by-step guide for US professionals on requirements, applications, and costs.